Energy Article – Who’s Who 2017[12248]

Introduction

Trinidad and Tobago is one of the many global Oil and Gas producers which have been hit hard by the precipitous drop is global energy commodity prices over the last two years.

One of the main drivers of this decrease in prices has been a dramatic increase in the supply of oil and gas from shale reservoirs among other things. There have been major discoveries, not only in the USA – who is now setting to become a dominant energy exporter – but also discoveries in East and West Africa, Israel and Lebanon, to name a few.

As a consequence world energy prices are not expected to rebound to pre- 2014 prices within the mid-term horizon.

This isn’t to say however that the energy business is no longer profitable. During the period of high prices, there was inflated demand for services and equipment, which drove costs up for energy services. New rigs, new seismic vessels etc. were built, while new supplies of steel and engineering services had to be added. The high prices allowed energy services companies to pay off financing and other operational / commercial debts. When prices dropped there was an oversupply, which has in-tern led to Exploration and Production (E&P) costs coming down by over 40% overall. Thus precipitous price decreases haven’t necessarily meant an equivalent precipitous drops in profitability for oil companies.

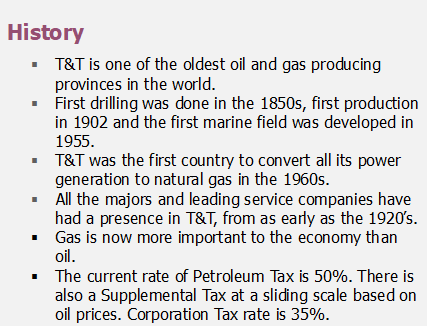

In Trinidad and Tobago’s case however, in addition to lower prices, production has also declined. This has meant significantly reduced taxation revenue for the Government, due to the make-up of Government’s fiscal regime regarding the Energy Sector. In order to incentivize activities to increase reserves and production, the government improved the taxation regime in favour of investors. Unfortunately, these have resulted in a reduction of government’s share of revenue, without the anticipated production or reserves increase.

Trinidad and Tobago – Potential Energy HUB for the Region.

Trinidad and Tobago is a natural hub for energy investments. This is due to the fact that it has significant installed base of infrastructure and skilled manpower, and very capable players in the energy services space. “The case for the country being used as a hub is easily made, as it’s easy to understand why you would utilise infrastructure that already exists, with [existing] capacity, rather than duplicating expenditures.” Said Norman Christie, Regional president, BP Trinidad and Tobago.

Trinidad and Tobago is a natural hub for energy investments. This is due to the fact that it has significant installed base of infrastructure and skilled manpower, and very capable players in the energy services space. “The case for the country being used as a hub is easily made, as it’s easy to understand why you would utilise infrastructure that already exists, with [existing] capacity, rather than duplicating expenditures.” Said Norman Christie, Regional president, BP Trinidad and Tobago.

Additionally, as a nation, the capital costs for all the investments that the country has embarked upon over the last 20 years is now generally paid for. Trinidad and Tobago has cheaper operating costs than almost any other country in the world. Additionally Trinidad and Tobago has had a history of operational excellence. For e.g. Phoenix Park, one of the largest gas processing facilities in Latin America and the Caribbean, has enjoyed an average 98% efficiency / plant availability over the last 24 years. The Natural Gas Company of Trinidad and Tobago (NGC) has never a major outage. Indeed there has been over the years a culture and capacity of excellence. There are approximately thirty (30) world scale natural gas plants which have been built in T&T, almost entirely with local labour, being delivered within budget and schedule.

One of the most recent and notable examples of Trinidad and Tobago’s capability was the completion of the fabrication of the topside of the Juniper Platform in-country at the fabrication yard at La Brea. Juniper is the largest platform structure ever fabricated in T&T and represents a US$ 2.1 billion investment by BP – an off-shore structure 12 stories tall (180 Ft) weighing just over five and a half thousand metric tonnes.

Politics and Labour Relations

One of the challenges that the Sector has been facing however is that of, at times, a changing and difficult political and labour relations climate in which to operate. Continuity of policy direction as well as continuing to ensuring that commercial operations are competitive, productive and cost efficient will be an on-going challenge.

Another item on the watch list for T&T is the issue of succession planning. Generally there has been a lack of adequate succession planning at the level of the state sector in particular. As such there is a threat that the industry may become starved of expert guidance, in-terms of the regulator, leadership, management, and to a lesser extent operations.

Short Term Outlook

There are more than adequate proven reserves of gas and oil to steady Trinidad and Tobago’s economy for years to come. There has been however an issue in terms of the level and timing of the investments needed to assist in producing those reserves.

From its current position, there are opportunities to apply new technology to monetising new smaller oil/ gas fields and getting more out of existing fields, through enhanced recovery methods. There is still much potential left.

Conclusion

While Trinidad and Tobago has so far had an enviable run in terms of its Energy sector, the country’s changing objective is now not only to increase GDP but also to reduce dependency on oil and gas. Increased use of technology and human capital development will be key ingredients for sustainability in the future. Additionally, T&T has to have an administrative regime – fiscal, regulatory policy – that reflects the maturity in some parts of the T&T basin (on-land and off shore), which reflects our experiences in the energy business – failings and successes – and which maximises the impact value and benefit to T&T citizens.

By Atiba Phillips, Principal Consultant at INFOCOMM Technologies Ltd (www.ict.co.tt)